You should own stock in your city

A radical idea for turning city residents into city shareholders.

This is a guest essay by Jeff Fong for Post Nation, seven writers exploring a world after nation-states. Support the project by collecting the series as a digital or print pamphlet 👇🏻

Shared Roof is a standard-looking mixed-use development in Seattle’s Phinney Ridge neighborhood: 35 residential units with some ground-floor retail and the amenities we usually see in new developments like this—a gym, bike room, and common spaces. Perfectly lovely, but seemingly standard fare.

But there is something different about Shared Roof, and that is its ownership structure.

The building was funded by ten friends who contributed the capital needed to bring the project to life. Those funders became shareholders in the legal entity that directly owns the building, entitled to dividends as the building generates revenue and to any appreciation in the value of their equity over time.

The really interesting part, though, is that several of the project’s investors are also tenants.

You might expect that to mean they just get a free unit. What actually happens is that they pay market rent, like anyone else, because their role as a shareholder is separate from their role as a tenant. As the building generates value, the corporate structure distributes it back to the people who collectively own it.

Shared Roof is one building on one street in one neighborhood, but the arrangement points toward something bigger: a different way of thinking about how we create, collect, and distribute the value that cities create.

Give me land, lots of land (value)

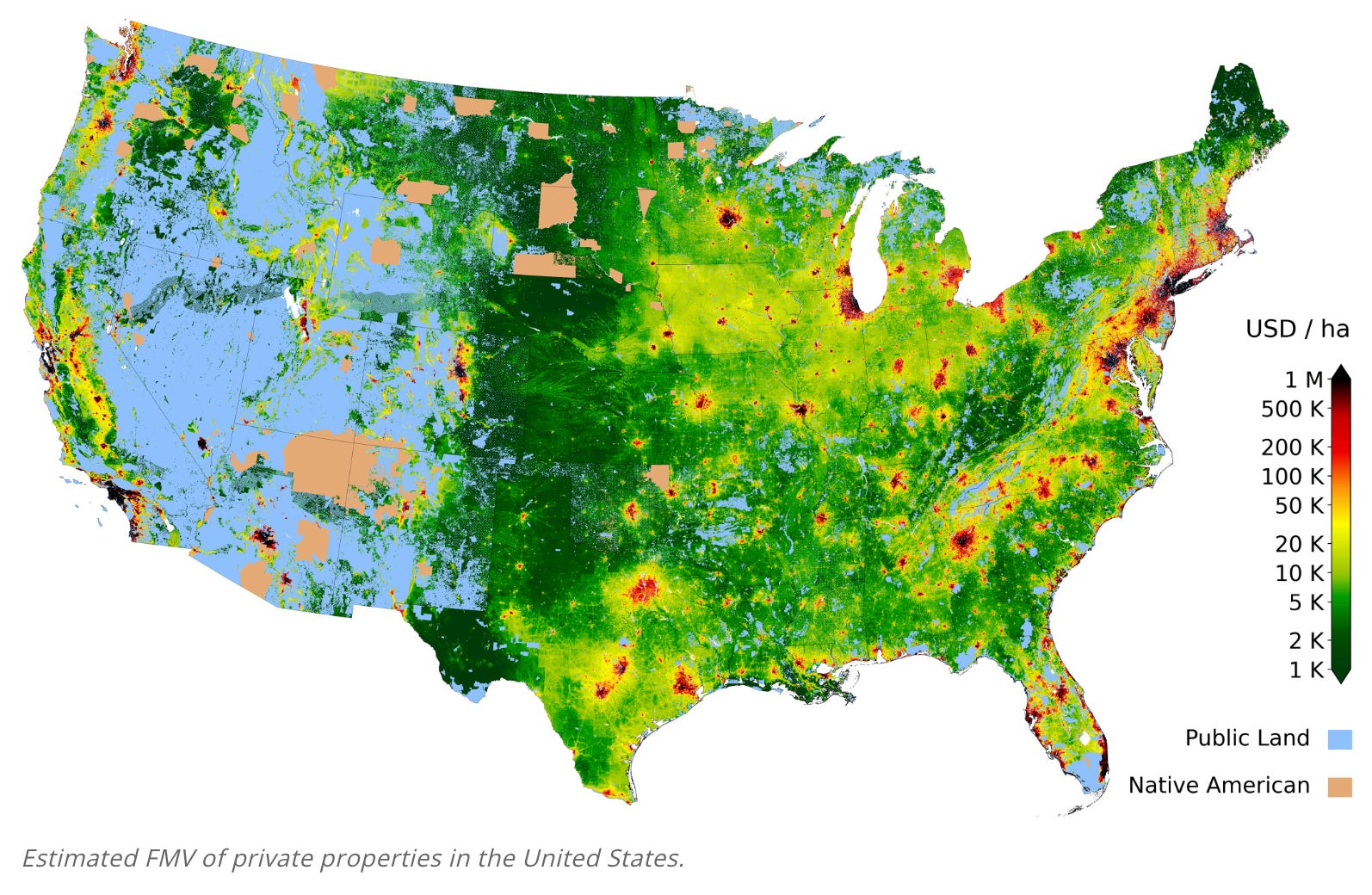

As a city’s economy grows, it becomes increasingly advantageous to live and do business there. More people and more money flow into the city, driving up the demand for space. As an economy grows, however, land becomes increasingly expensive.

More people making more money cluster in places of opportunity, in part because of everyone else who went there before them and made it a great place to be. This is what economists call agglomeration effects. Perhaps a more accessible way to think about it is as a house party—a party is only as good as the people who show up.

While municipal governments don’t unilaterally control this dynamic, they’re also not just along for the ride. They provide generalized services like sanitation and law enforcement, creating the broad conditions upon which urban growth depends. Local governments drive land values in more direct, localized ways as well. Transit stops increase adjacent property values everywhere from New York to Hong Kong to Paris. Other location-specific amenities like public parks or high-performing public schools have the same effect. The decisions a city government makes about where to invest, what to build, and how to govern itself shape the conditions under which agglomeration either flourishes or stagnates. And those conditions show up, reliably, in land values.

If we understand municipal wealth as really being land value, then the two most straightforward ways for a city government to monetize that value are either land value taxation or municipal land leasing—taxing land people own or leasing out land that belongs to the city. Both work on the same basic insight: when a city grows and the municipal government makes good investments, land becomes more valuable. A municipal government should fund itself from all that value it’s helping to create.

Think about what happens when a new subway station opens. The land around that stop becomes more valuable because it becomes functionally closer to everything else. A land-based revenue model looks at this and says that the value creation enabled by public infrastructure and created by the community as a whole ought to be collected and deployed in the public interest, not privatized by landholders who were simply lucky enough to buy into the dirt somewhere first.

Fully implemented, this creates a virtuous cycle. The municipality collects land value, makes public investments to increase land value, and leaves other types of economic activity relatively untouched (meaning more economic growth and…you guessed it, higher land values). The shift to land-based revenue itself also tends to increase land values — by removing the tax penalty on development and concentrating holding costs on unproductive land, LVT encourages denser use of urban space, which drives up the very base the city is drawing from. The act of switching increases the value of the very asset the municipality uses to fund itself.

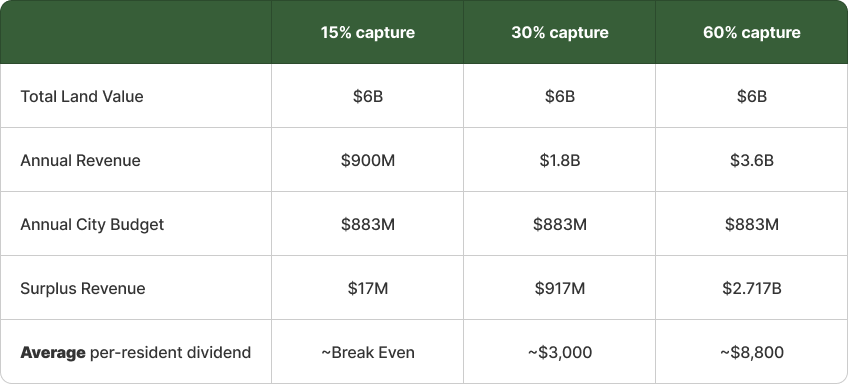

And yes, it’s plausible to imagine a city could make most of its money by monetizing land values. The City of St. Paul, Minnesota sits on over $6 billion in taxable land value.1 Its annual budget is around $883 million. If the city collected 15% of that total land value every year, it would more than cover current expenditures.2 So the business model makes sense and, if this all still seems too fanciful, it’s also just how a mall works.

Ok, back to Seattle. Shared Roof created value by building something that added value to the neighborhood and the city. This is what governments do on a municipal scale. But Shared Roof also remits that value back to tenant shareholders. Let’s talk about how a city could do the same.

Collective ownership of urban life

Imagine a city where residents own shares in a municipal corporation. The corporation generates revenue by monetizing land value (again, by either taxing privately-held land or leasing publicly owned holdings). Excess revenues, after the city’s operational needs are met, flow back to residents as dividends.3 The more shares a resident owns, the larger their stake in the proceeds of the city’s economic growth. And just like a corporate board, the management put in place by the shareholders — a mayoral administration and council members elected by the city’s residents — would be responsible for navigating the tradeoffs between bigger investments and more generous dividends every year.

The key departure from conventional shareholding is how people come to own their shares. In our Shared Roof example, ten friends put in capital and got equity accordingly. Their ownership stake was commensurate with their financial investment. That logic makes sense for a building, but applied to a city, it would simply recreate the wealth inequality we already struggle with today. After all, allocating the lion’s share of municipal wealth to whoever had the most money in the first place hardly seems like much of a change. Instead, my idea is a system in which shares accrue based on tenure. The longer a resident lives in a city, the greater their stake and the more upside they gain from ongoing growth.

Let’s suppose we structure this using a vesting schedule (i.e., a system that grants an increasing number of shares over time). A resident would receive an initial tranche of shares at the age of majority, setting them up to begin adult life.4 Shares would then incrementally accrue each year of residency with a final significant tranche at retirement. This would ensure retirees could actually retire.

For residents who move away, vesting pauses (analogous to a leave of absence at a company with equity compensation). For those who arrive later in life, their schedule is pro-rated.

Shares would carry one right only: a proportional claim on excess municipal revenue. Not voting rights, not governance power. The motivating idea is to create a system of economic ownership operating in parallel with political enfranchisement. Shares would also be non-alienable and non-bequeathable. If they could be sold or inherited, it would take only a few generations for the city’s financial upside to concentrate in a small set of hands.5

A rising tide that lifts all ships

So, what is all this actually for? A way to share in the wealth that cities create that’s not just more equitable, but also pro-growth.

A land-based revenue model reorients municipal governments toward growth. Transit infrastructure, a quality public education system, and even just a competent administrative apparatus that makes things like getting a business license easy all support economic activity and, ultimately, drive up the land values the city monetizes to fund itself.

And this isn’t just an incentive story. It’s an epistemological one. Land values function as a price signal for public investment. A road doesn’t have to be a toll road to generate revenue; if it increases the value of surrounding land, a municipal government would have a legible way to tell whether its spending was actually working.

The more consequential shift, though, is what this does to residents.

Middle-class Americans rely on home values as their primary vehicle for wealth accumulation. And home values, as we’ve established, are really land values. The problem with the way we do things today is that we distribute upside based on who happened to buy the right piece of dirt at the right time. The system is haphazard, exclusionary, and creates all the wrong incentives. A homeowner whose wealth is tied up in their property value has rational reasons to oppose the very things that drive broader urban growth: New housing might be a threat to free street parking. Infrastructure might require increased property taxes. When the change that growth requires comes with no upside for property-owning incumbents, the incumbents have every reason to fight it.

We built a system based on individualized land speculation, and it’s created a relationship to urban growth that’s short-term and myopic. What this shareholder idea is meant to tease out is how we might align people’s preferences with the entire city. When a new apartment building down the street is part of what keeps the city growing (and residents’ dividends along with it), people have a reason to welcome their new neighbors. When people aren’t anchored to a specific parcel they’re hoping will appreciate enough for them to retire off of, their attachment to place becomes an attachment to the city as a whole — instead of a parochial fixation on only a couple blocks.

Similarly, this would lead to residents understanding and supporting longer-term investments. Policymakers would have a much easier time selling residents on longer-term investments if they could credibly promise that every new public investment will benefit them. A new public school benefits residents without children. A commuter rail extension matters even to people who don’t use it. Both increase land values, and therefore dividends. The system gives everyone a way to share in the upside.6

Beyond the welfare state

It would be easy for some folks to read all of this as an elaborate way of doing a universal basic income. But the ideas here aren’t intended to motivate mere redistribution. They’re proposing a different way to think about collective wealth.

Consider the Alaska Permanent Fund. It’s a sovereign wealth fund, seeded by oil revenues and managed by the state, that pays an annual dividend to every qualifying Alaskan resident — roughly $1,000 per person in 2025. Alaskans do not understand this arrangement as welfare. They understand it as a form of collective ownership. This is the relationship I imagine residents would develop with the institution of shareholder ownership. And really, I’d imagine that relationship developing even more strongly.

Alaska’s oil sits in the ground whether any human has done something or not. A city’s land value, that reflection of demand to be in a place, exists because of everything everyone in a city has contributed. The businesses that create the job market, the employees that make the business possible—the art, music, and broader cultural life that economic activity makes possible—exist because of everyone’s collective participation. A party is only as good as the people who show up, and I’d say the same is true for cities. Shareholder ownership recognizes all of that, and ensures the people who make a city great get to share in everything they’ve collectively built.

This is a thought experiment, but it’s a hypothetical whole made out of actually existing parts. Land value capture (whether of the LVT or municipal leasing variety) exists and is only becoming more popular. Sovereign wealth funds are quite real. And, of course, shareholder forms of ownership are commonplace. So perhaps building blocks are more readily available than they might seem.

In the immediacy though, I hope this conversation helps us better appreciate the contours of the problems we face and begin thinking more radically about the types of solutions we could build to carry us into the early days of, if not a better nation, then perhaps just a better world.

Land Value Return in St. Paul, MN, Center for Land Economics.

That figure is an understatement as it doesn’t include publicly held land that could be monetized through leasing.

The most famous companies today don’t distribute profits to shareholders (or do so in minimal amounts). The prevailing theory is that it’s better for management at successful companies to reinvest profits back into making those companies even more successful (and, therefore, the equity held by investors even more valuable). So, if shareholders getting paid a portion of company profits doesn’t sound familiar, it’s because I’m reaching back to an older, simpler version of corporate shareholding.

We could haggle over different criteria for establishing residency. Most US cities base this purely on whether your declared primary residence is within their borders. For our purposes, we’re imagining a system that gives people a part of the value they create by contributing to the local economy; so, finger in the wind, a six month residency period seems reasonable (i.e. a new adult resident would receive their first tranche of shares 18 months after moving to their new city).

And remember, everyone gets their own shares. Shareholding would pull land value out of a system where land as wealth gets passed down along family lines and, instead, distribute that value to everyone in the here and now.

One caveat worth noting: as residents approach retirement, they may prefer larger dividends today over infrastructure investments that pay off over decades. This could amount to a near-term bias the system doesn’t fully solve, even if incentive problems are much improved over the world we live in today.

| A guest post by

|

The City of Edinburgh (Edinburgh Council) is introducing this in September. Not for everything - focusing on greener initiatives I think. But interesting to see it starting.

This idea appeals to me because it treats residents as actual participants in the value of a city, not just consumers of services or obstacles to development. So much urban wealth comes from the collective life of a place: the workers, the schools, the small businesses, the transit, the culture, the people who stay long enough to make a city feel like itself.

Right now, too much of that value gets captured by whoever bought the right patch of dirt early enough. This idea feels powerful because it asks a better question: if residents help create the city’s value, why shouldn’t they share in its growth?

I also like that the proposal rewards tenure without turning the shares into another inherited asset game. That matters. Otherwise, we just reinvent the same inequality with shinier paperwork, and please, we already have enough expensive nonsense wearing a reform costume.